An Opinionated Onboarding Setup for New Hires at Microsoft

Note: I no longer work at Microsoft, and this article is no longer kept up-to-date.

Welcome to Microsoft! I’ve written this guide to reduce decision fatigue about what to do during onboarding. This information complements what you already receive during New Employee Orientation (NEO). As I get recurring questions from new hires, I’ll update this guide accordingly. (If you’re not at Microsoft, this page isn’t particularly useful for you.)

Some assumptions:

- You work at Microsoft in Redmond or the Puget Sound area.

- You will primarily invest in tax-sheltered accounts, with checking, savings, or money market (

SPRXX) accounts for everything else. - You have an emergency fund for 3-6 months of expenses in place (if not, prioritize building your emergency fund before investing).

- You will pay for your day-to-day expenses almost entirely through bonuses and stock (both RSU and ESPP) until you hit your tax-sheltered limits, redirecting your base salary to retirement.

- You prefer a set-and-forget approach to managing your life instead of day-to-day management.

Initial Day-to-Day Life Setup

Rename your alias. Usually, you’ll need to change your automatically-generated alias (for example, tibari to tbarik, internal link). You’ll want to follow the Microsoft account naming conventions (“intuitive aliases”) , which basically means some combination of letters from your first and last name. The naming conventions aren’t strictly enforced (and Microsoft Research has an explicit exemption), but colleagues find it pretentious when people choose exotic aliases. Do this as early as possible.

Your canonical e-mail address is usually firstname.lastname@microsoft.com. Although you can be e-mailed at your alias, the canonical e-mail address is what you should give to others outside Microsoft.

Machine setup. On the first day, you’ll need to reformat your workstation and laptop using PXE boot, through the corporate network. Alternatively, you can install a fresh Windows 10 Enterprise image, and then join the domain. Don’t try to join the Microsoft domain using an OEM Windows installation. Name your computers such that they contain your alias (for example, tbarik-ws).

Activate subscriptions. As a Microsoft employee, you have complementary access to some amazing learning resources, including PluralSight and O’Reilly Online Learning. You should also go ahead and activate your subscriptions to the New York Times, Wall Street Journal, and a few others (Microsoft Library, internal link).

Professional membership dues. For researchers (technically I think anyone can do this though), you should expense your ACM and IEEE membership fees. Microsoft’s digital library also includes access to the ACM and IEEE libaries, so don’t pay for those again.

Corporate American Express card. This card takes a while to receive, so go ahead and activate it early (internal link). You only need this card if you travel somewhat frequently.

Visual Studio Online. Login to Visual Studio Online with your Microsoft account and activate your $150 personal monthly credit. Do the same for Office.

Blind. You can finally join Blind (yay?), which has an anonymous community for Microsoft. Yes, Blind is toxic, but it’s sometimes the only way to get an unfiltered lens of the company. Use sparingly.

Outlook rules. You will receive far more e-mail that you can actually manage. I only have three types of simple Outlook rules. First, for each Discussion list, I create a separate rule and folder. Second, I create a priority rule such that any e-mail from my manager or above goes directly to my INBOX (which triggers notifications). Third, everything else goes to a folder called Quiet, which I only check periodically (notifications suppressed).

Personal use. This is a surprisingly common question, so I just looked it up directly: “You may use Microsoft devices, networks and systems for personal use if it does not interfere with your job responsibilities or negatively impact corporate resources.” A separate policy says no pornography or pirated software. There are certain workstations, called Secure Access Workstations (SAW), which have a much stricter usage policy.

Matching donations. Each year, Microsoft will match up to $15000 of your donations, dollar-for-dollar. You can setup recurring donations (deducted directly from payroll) towards your most important causes through the giving portal.

Financial

Here’s how I setup my finances, if you want to do the same. Consult a financial planner for your specific situation.

This section reads like a Fidelity advertisement, but that’s mostly because Microsoft offers their 401k, ESPP, and stock awards through Fidelity.

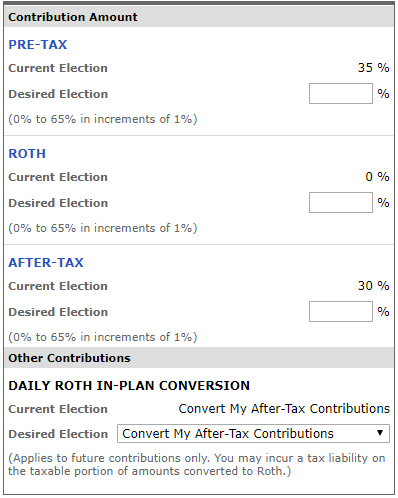

Fidelity 401K. You will fund your 401K through both pre-tax and after-tax dollars. The pre-tax contribution limit is $19500 with a 50% match by Microsoft ($9750, also in pre-tax dollars). You should also do after-tax contributions to $28750, and for this you will do a daily Roth in-plan conversion to minimize tax burden.

The maximum total payroll deduction allowed for all sources is 65% of gross income per pay period. Microsoft will stop contributing automatically once you hit the IRS limits. Here’s a reasonable allocation:

To reach these targets, you will rely on selling Microsoft stock and using your cash bonuses for day-to-day income. For at least the first part of the year, your actual paycheck will be relatively tiny, since a significant chunk of your paycheck is redirected towards retirement.

If you start later in the year, for example September, you may need to be even more aggressive: ramp up the pre-tax contributions all way to 65% until you reach the maximum Microsoft match, then swing back to 65% for after-tax. Depending on when you start, it may not be possible to reach the after-tax limit in the first year.

The target date funds offered in this plan are really good (0.06% expense ratio). Pick one of the BlackRock LifePath index funds (based on your expected retirement age, mine is BTC LP IDX 2050 N) and put 100% in that fund. If you want to do something more sophisticated, join Microsoft’s invclub.

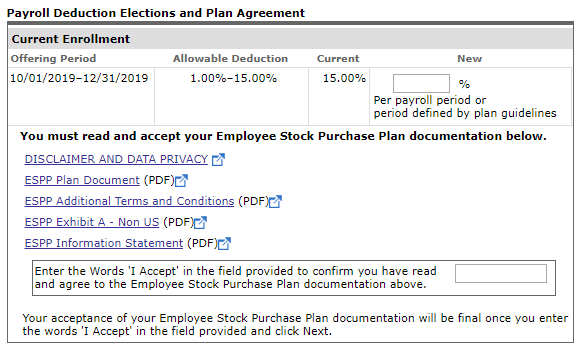

Employee stock purchase plan (ESPP). The ESPP plan is through Fidelity NetBenefits. Set your ESPP contributions to 15%. Your discounted (10%) stock purchases are limited to $25000 per year (well, essentially). You will automatically be refunded if you overfund your ESPP plan.

Sell your Microsoft stock the day you receive it and use it for income. The reason is that you are already overleveraged in Microsoft just by virtue of working for them.

Backdoor Roth IRA. Your income will likely be too high to contribute to a Roth IRA directly. But you can do a rollover, which basically works like this: open a Traditional IRA and a Roth IRA, then put $6000 in your Traditional IRA. As soon as the funds settle, do a rollover from your Traditional IRA to your Roth IRA.

If you have a non-employed spouse and like them, they too should have a Traditional IRA and a Roth IRA. Repeat the process ($6000) for a total of $12000 a year. But note that the money becomes theirs (the “I” in IRA is “Individual”).

There are some hurdles if you already have pre-tax accounts, in which case you’ll have to shuffle some accounts around first.

I do Boggleheads-style investing for the Roth IRA, with the funds FZROX (0% expense ratio), FZILX (0% expense ratio), and FXNAX (0.025% expense ratio).

Fidelity supports a backdoor Roth IRA out of the box: just do a Transfer from the Traditional IRA account to the Roth IRA account.

Other Fidelity odds and ends. Open a Fidelity Cash Management Account (basically, it acts like a checking account) and use it as your primary account. Direct deposit your pay to this account. You’ll have access to your pay a day early if you use Fidelity. Fidelity also has a nice Rewards Visa Signature card, for which you would now be eligible. Setup extra login security with the Symantec VIP access app.

Annual stock awards and special stock awards. You have a choice of two brokers, Morgan Stanley or Fidelity. Pick Fidelity. Like ESPP, sell your stock the day you receive it and use it as income.

These are announced in September. If you join Microsoft after March 31st, you won’t be eligible for rewards or bonuses until next year’s cycle. You will be eligible for a prorated merit increase (basically, cost of living adjustment).

529 plan. If you still have income left over, consider a 529 plan.

Open Enrollment

Just a few more items left around open enrollment. For almost all of these, I think the defaults are okay.

ARAG. Microsoft offers a group legal service, ARAG, which has gotten me out of a few traffic violations already. You also get credit monitoring through ARAG.

Health insurance. Both health insurance plans are reasonable. The HSA works a bit better if you’re single and don’t expect to have any health issues, while the Kaiser Permanente plan works a bit better if you have a family and have a Kaiser Permanante hospital nearby.

FSA. If you pick the Kaiser Permanente plan, you can utilize an FSA. If you don’t know how much to contribute, set this to $500, and adjust the following year as needed.

Other Benefits

Xbox Game Pass. A free 12-month subscription to Xbox Game Pass Ultimate.